There is a chart I want you to look at before we talk about anything else.

It is the OECD Composite Consumer Confidence Index for the United States, sourced from the Federal Reserve’s FRED database. It tracks how Americans feel about the economy, their finances, and their prospects — going back to the early 1960s. It is one of the most reliable leading indicators of how people make major financial decisions, including real estate ones.

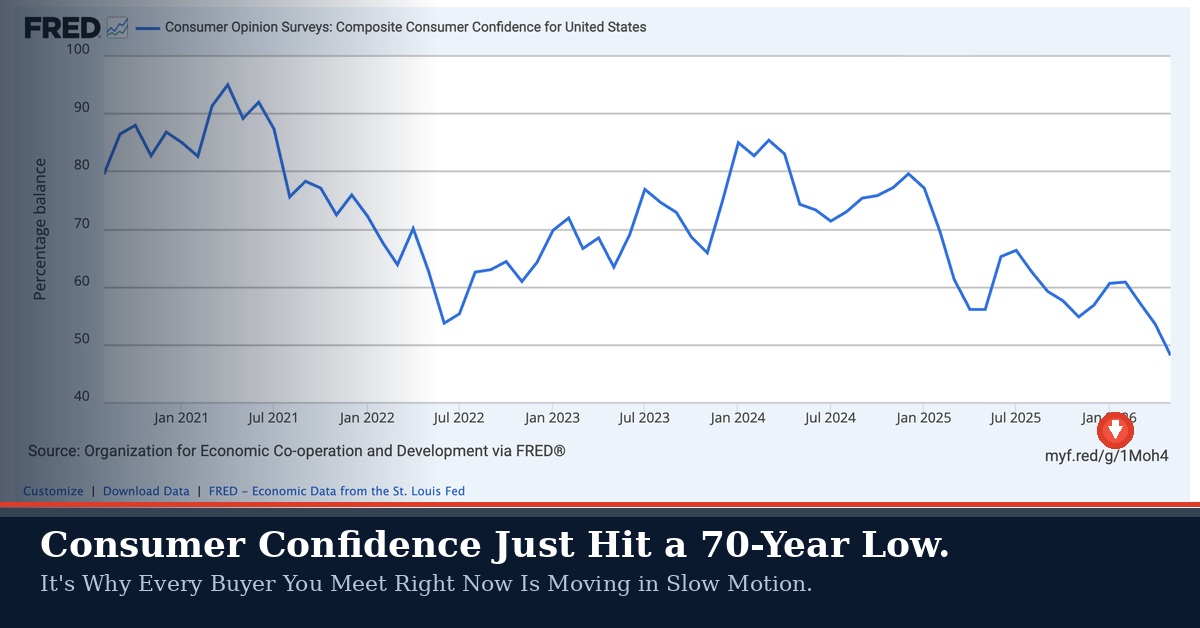

The chart shows a line that peaked near 95 in early 2021, dropped sharply through 2022 as inflation arrived, partially recovered through 2023 and 2024, and then — starting in 2025 — fell off a cliff. As of May 2026, the composite index sits just below 48. It is still falling.

That number is not just low. It is historically extraordinary. It is lower than the bottom we saw during the 2020 pandemic shock. Lower than the depths of 2022 when inflation first hit. Lower than any reading in the post-financial-crisis era.

Let that land. Americans are currently less confident about their economic future than they were when the entire economy was forcibly shut down.

If you have noticed that buyers are slower, more deliberate, more likely to pause mid-search, or to ask more questions than they used to, this chart explains it. It is not about your property. It is not about mortgage rates. It is about something deeper and harder to fix quickly: people have lost confidence in the future’s predictability.

What the Consumer Confidence Index Actually Measures

The composite index is a combination of several survey components: how people feel about current economic conditions, how they expect conditions to change over the next twelve months, whether they think it is a good time to make major purchases, and how secure they feel about employment.

Think of it as a dashboard reading of the national mood — not a single emotion, but five different ones averaged together. When the index is high, people feel that conditions are good and the future is bright. They move forward with confidence on major decisions. When it is low — as it is now — they hesitate. They ask more questions. They pull back. They wait.

The University of Michigan’s Consumer Sentiment Index hit a record low of 44.8 in May 2026 — the worst reading in the survey’s seventy-year history. Even with a modest June recovery to 48.9, sentiment remains 13% below January 2026 and 19% below a year ago. The Conference Board’s Consumer Confidence Index fell to its lowest level since May 2014 — surpassing its depths during the COVID-19 pandemic — as all five components of the index deteriorated simultaneously.

The direction of these indices matters as much as the absolute level. A low reading that is improving sends one signal. A reading that is still falling — as ours is — sends another.

Why This Collapse Is Worse Than COVID

This is the question that should be driving real estate conversations right now, and almost nobody is asking it directly.

During COVID, consumer confidence crashed fast and hard. But the causes were visible, specific, and — critically — temporary. A virus. A shutdown. Policy responses were immediate and massive. Within months, the source of the anxiety was known, the government response was underway, and the path back to normal, however uncertain, was at least conceivable.

What is driving confidence down today is different in kind, not just in degree. It is a confluence of pressures that do not have a clear resolution date.

Two-thirds of consumers report cutting back on spending due to rising prices. Most of those cutting back are delaying expensive purchases—not avoiding them forever, but pushing them out. Year-ahead inflation expectations sit at 4.6%, substantially above the 3.4% reading seen in February before the Iran conflict began. Decreases in sentiment are being seen across every political party, income level, age group, and education level. This is not a partisan mood or a demographic anxiety. There is a broad-based national feeling that the ground is unstable.

The triggers are layered in ways that are hard to disentangle. Energy prices surged with the Iran conflict and fed through to everything — groceries, utilities, transportation, and manufacturing costs. Tariff uncertainty has been a persistent background noise for over a year. Federal job restructuring has added anxiety among workers in government-adjacent industries. And now Warsh’s Fed has added a new layer: the possibility of rate hikes, not cuts, on the horizon.

Each of these factors, individually, would be manageable. Together, they create something the NAHB’s chief housing economist summarized in a single word: instability. “It all comes down to one word — stability. Stability from policymakers. Stability in the labor market. Stability in interest rates. Stability in home prices.”

Right now, consumers have none of those four things. That is the chart.

What This Looks Like in the Real Estate Market

One housing economist described it directly: consumers are acting with extreme caution, waiting for lower rates, more stable inflation, and more certainty. The erosion of confidence is creating a “psychological freeze” in the housing market that extends beyond interest rates.

That phrase — psychological freeze — is the most accurate description I have heard of what I am seeing on the ground.

The typical US home spent 64 days on the market in January 2026, the longest time on the market in six years. About 20% of current homebuyers paused their search at some point over the past two years before re-entering the market — and when they came back, they were cautious but motivated, maintaining budgets similar to those in their initial search.

These are not buyers who have given up. They are buyers who are moving more slowly and deliberately than at any point in recent memory. They are requesting inspections that they might have waived three years ago. They are negotiating harder on price. They are taking two or three showings before making a decision that they once would have made in one. Rather than focusing solely on finishes and floor plans, today’s buyers are evaluating how a property might perform over the next five, ten, or twenty years — reassurance that the neighborhood will remain desirable, that demand will continue, and that future buyers will want what they are buying today.

This is not irrational behavior. It is a rational response to a genuinely uncertain environment. These buyers have not lost interest in owning. They have lost confidence in the clarity of the timing.

What It Means for Boston and Cape Cod Specifically

Boston’s luxury market has a structural advantage in this environment that most markets do not: necessity. Corporate relocations, career transitions, family changes — these buyers have to move regardless of how they feel about the economy. Necessity-driven demand does not freeze. It slows, it becomes more deliberate, but it does not stop.

What freezes in Boston is discretionary demand — the buyer who is perfectly comfortable where they are and is considering an upgrade. That buyer, in a low-confidence environment, stays put. This is why Boston’s luxury market has seen days on market lengthen, and why properties priced for the market as it was rather than the market as it is are sitting longer than their sellers expected.

Cape Cod is more exposed to the confidence collapse than Boston, for exactly the reason you would expect: Cape Cod is almost entirely a discretionary market. Nobody has to buy a second home. That purchase is made from a position of confidence — confidence in personal financial stability, confidence in the market, confidence in the future. When all three of those are shaken simultaneously, discretionary purchases get postponed first.

This is not a permanent condition. The buyers who are pausing right now are not disappearing — some are moving forward while others are waiting in the wings should conditions improve. The Cape Cod inventory of genuinely exceptional properties remains finite. The buyers sitting on the sidelines today will return when one or more of the confidence variables shift — when inflation shows sustained progress, when the rate outlook stabilizes, when the geopolitical picture clarifies.

The sellers who understand this dynamic — who price for the buyers who are in the market right now, not the buyers who were in the market two years ago — are still transacting. The sellers who are waiting for confidence to fully recover before adjusting their expectations will be waiting a long time.

What Buyers in a Low-Confidence Market Should Know

Your hesitation is legitimate. The data support it. The environment is genuinely uncertain in ways that are different from normal market cycles.

But here is what thirty years in this market has taught me: the buyers who wait for confidence to fully recover before acting almost always look back and wish they had moved sooner. Confidence recovers when conditions improve. When conditions improve, more buyers re-enter the market simultaneously, competition increases, and the window of negotiating leverage that exists today — when fewer buyers are competing for the same supply — closes.

The buyers who do best in low-confidence environments are not the reckless ones who ignore the signals. They are the disciplined ones who use the environment to their advantage: buying with more leverage, more time, more due diligence, and less competition than they would find on the other side of a confidence recovery.

If you are a buyer who has been deliberate, cautious, and slower than you expected, you are not behind. You may be exactly where the market needs you to be right now. The question is whether you are using this environment strategically or just waiting.

That is the conversation worth having.

508-420-8800 · thegriffin.co

Griffin Realty Group serves buyers and sellers across the Boston metro and Cape Cod luxury real estate markets.