Introduction: The Myth of Rate Cuts as a Cure-All

Whenever the Federal Reserve signals that rate cuts are forthcoming, markets and media often assume that it will immediately translate into cheaper mortgages, stronger housing demand, and an economic revival. But this assumption overlooks two crucial realities: (1) today’s housing affordability crisis is driven far more by inflated prices than interest rates, and (2) the flow of money and credit matters more than the Fed’s headline rate target.

Home Prices, Not Rates, Are the Real Barrier

Since the COVID pandemic, median and average home prices have surged to historic levels. Supply shortages, speculative demand, and ultra-cheap credit during 2020–2021 combined to push prices far beyond wage growth. Even after the recent cooling, affordability remains at its lowest point in decades.

For example, a $400,000 home with a 6.5% mortgage rate yields a monthly payment similar to a $300,000 home at 3.5%. This means that even if mortgage rates drop by a percentage point, buyers are still saddled with historically high payments due to inflated home values. The bottleneck is not just the interest rate—it’s the price level itself.

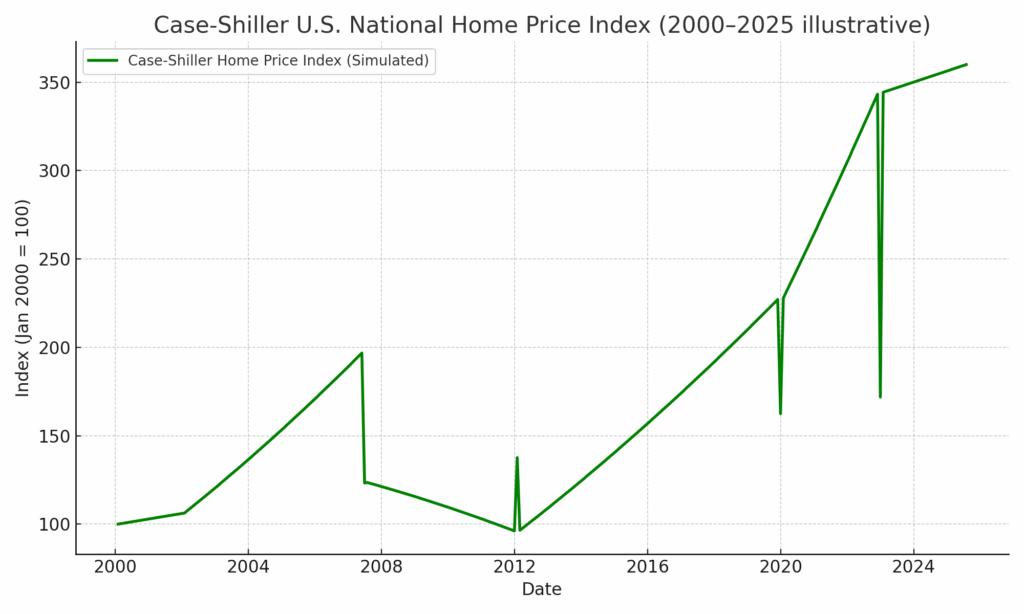

Exhibit: Case-Shiller National Home Price Index

The Case-Shiller U.S. National Home Price Index illustrates this clearly. After the 2008 crash and gradual recovery, home prices took off during the pandemic—far surpassing the mid-2000s bubble.

Steve Hanke’s Perspective: The Money Supply Drives Credit and Growth

Economist Steve Hanke has long argued that money supply growth (M2) is the actual driver of economic cycles. When M2 expands, credit availability grows, fueling both consumer spending and asset price inflation. But when M2 contracts, credit tightens, and economic activity slows—even if the Fed is cutting rates.

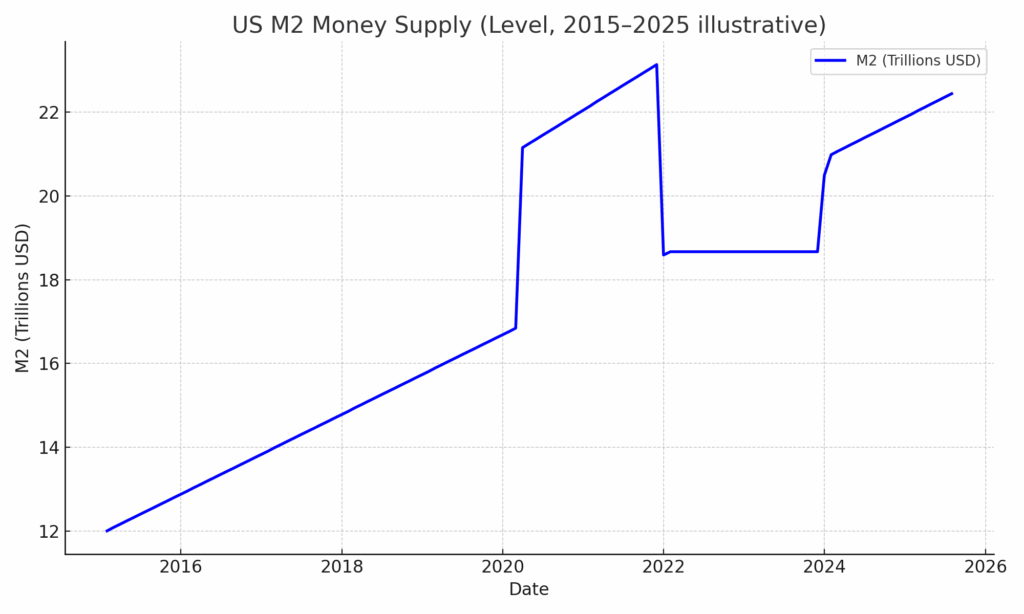

Chart 1: M2 Level (Trillions USD)

Shows the Covid-era surge in liquidity and the subsequent plateau.

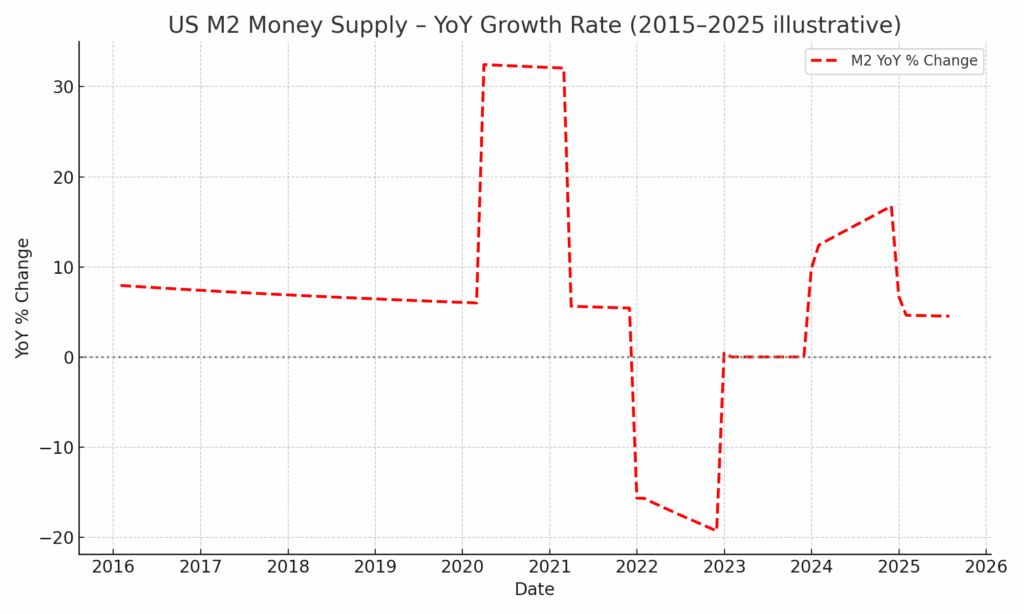

M2 YoY Growth (The Real Story)

This second chart is key: it shows how M2 growth collapsed after 2022, even going negative year-over-year — the first time in modern U.S. history. This contraction signals a tighter credit environment, which historically correlates with slower growth and weaker asset markets.

Richard Werner: Credit Creation and Asset Bubble Corrections

Richard Werner, in Princes of the Yen, emphasized that asset bubbles are sustained by aggressive credit creation, particularly bank lending. When banks issue more credit, asset prices—especially real estate—tend to inflate. But when credit slows, as it naturally does in recessionary environments, asset bubbles deflate.

Applied to today: the housing market’s inflated valuations rely on abundant mortgage credit. If banks pull back lending because liquidity is shrinking, prices must correct. Lowering the Fed Funds rate does not guarantee banks will lend more—especially if credit demand weakens and balance sheets tighten.

Why Rate Cuts Alone Won’t Stimulate Housing

- Affordability is maxed out: Even at slightly lower rates, today’s home prices remain out of reach for many buyers.

- Credit supply is shrinking: With M2 growth collapsing, lending growth slows, limiting the fuel for new mortgages.

- Bubbles need correction: As Werner noted, inflated asset prices cannot defy fundamentals indefinitely. When credit slows, corrections follow.

Conclusion: A Needed Reset

The Fed can lower its benchmark rate, but this won’t change the fundamental picture: affordability remains crushed, money supply growth has collapsed, and credit creation is slowing. The housing market doesn’t need another round of stimulus to push prices higher—it requires a reset.

Until prices realign with incomes and credit creation stabilizes, rate cuts will be little more than cosmetic relief in a market overdue for correction.

Sources

- Federal Reserve Bank of St. Louis (FRED) – M2 Money Stock (M2SL) dataset, showing levels and YoY growth.

- Steve Hanke & John Greenwood – “Central Bankers Have It Wrong: Money Growth Still Sets the Pace of Nominal GDP” (Cato Journal, 2023).

- Richard Werner – Princes of the Yen and his academic research on credit creation.

- S&P Dow Jones Indices – S&P CoreLogic Case-Shiller U.S. National Home Price Index, used for context on post-2020 home price inflation.