Conventional wisdom says that when the Federal Reserve cuts interest rates, the housing market breathes a sigh of relief—mortgage rates fall, buyers rush in, and prices hold steady. But economist Richard Werner has spent decades challenging this assumption. His research shows that interest rates don’t lead the economy—they follow it. When growth slows, rates fall in response, but lowering rates doesn’t guarantee a revival.

Pair this with Robert Shiller’s CAPE ratio, which signals dangerous overvaluation in equities, and you have a sobering warning: both real estate and stock markets could be poised for sharp corrections, no matter what the Fed does.

Werner’s Reversal of the Narrative

Werner, best known for developing the “Quantity Theory of Credit,” flips the usual Fed narrative on its head. Instead of rates being the steering wheel of the economy, he argues they’re more like the rearview mirror—a reflection of what has already happened.

This insight has significant implications for real estate:

- Cuts don’t cause growth: If rates are falling, it likely means demand and credit creation are already weakening.

- Lower bank margins mean tighter lending: Cheaper rates squeeze banks’ profits, making them less willing to lend. That can reduce the availability of credit for mortgages—the opposite of what homebuyers expect.

- Asset prices become more fragile: When housing markets are already inflated, reduced credit creation can expose just how dependent values are on fresh lending.

In short, Werner suggests that rate cuts are a symptom, not a solution—and that’s a message Boston and Cape Cod homeowners should heed. His perspective carries weight not only from his academic research, but also from his analysis of Japan’s 1990s housing bust—an era when low rates failed to stop property values from collapsing.

Boston & Cape Cod: A Price Surge Built on Sand

Take Massachusetts.

- Boston proper has seen its median sale price push above $1 million in Greater Boston, while listings within city limits hover between $825,000–$895,000, depending on the source. That’s historically high and leaves little room for error.

- On Cape Cod (Barnstable County), the median home price has climbed steeply as well, rising from under $500,000 a decade ago to nearly $1 million today.

These numbers tell a story of scarcity, demand, and speculative fervor. But if Werner is correct, the Fed’s next move won’t cushion these markets—it may simply reveal how overextended they’ve become.

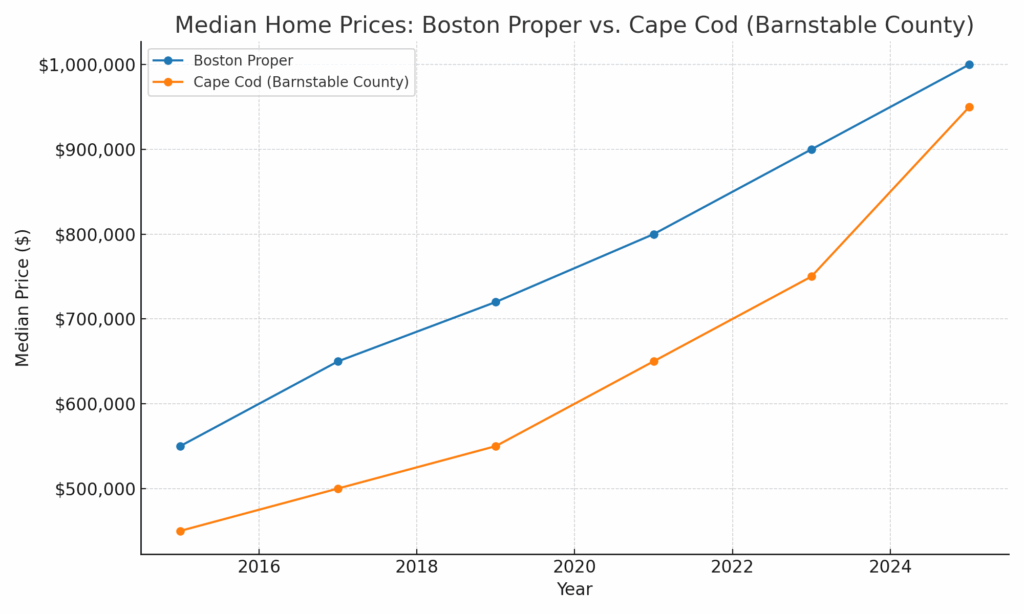

Visualizing the Surge

To see just how dramatic the climb has been, compare median prices in Boston and Cape Cod over the last decade:

Both lines tell the same story: steep, sustained growth. But Cape Cod’s rise has been particularly sharp, leaving it more vulnerable if credit dries up and demand falters.

Shiller’s CAPE: Echoes From the Stock Market

Meanwhile, Robert Shiller’s CAPE ratio offers a parallel warning. With the CAPE sitting near 38, more than twice its historic median, equities look dangerously stretched. Historically, such readings predict muted or even negative returns over the following decade.

Just as housing depends on credit creation, stocks depend on earnings relative to prices. Both are flashing signals of overvaluation. Together, Werner and Shiller highlight a looming reality: whether in real estate or equities, asset prices can’t outrun fundamentals forever.

The Takeaway

“Rate Cuts Aren’t a Sanctuary” isn’t just a catchy phrase—it’s a framework shift. Werner reminds us that falling rates are the rearview mirror of a slowing economy, not the steering wheel guiding it forward. Shiller’s CAPE reminds us that markets inflated beyond fundamentals eventually reset.

For homeowners and investors in Boston, Cape Cod, or the broader U.S., the message is clear: don’t count on the Fed to bail out housing or stocks. If these economists are correct, the real story is not what rate cuts will do, but what they reveal—that the economy, and the asset markets tied to it, may already be heading for a reckoning.